Why You Should Invest for Retirement and How Inflation Can Impact Your Future

Investing for retirement is not just a smart move. It is essential. With longer life expectancies and rising costs, having a robust retirement plan in place is more crucial than ever. One of the biggest threats to your retirement savings is inflation, which can quietly erode your purchasing power over time.

The Power of Investing for Retirement

Investing is the cornerstone of a successful retirement plan. It allows your money to grow over time, taking advantage of compound interest and market returns. While saving is important, simply stashing cash in a savings account will not provide the growth needed to outpace inflation or sustain you through decades of retirement.

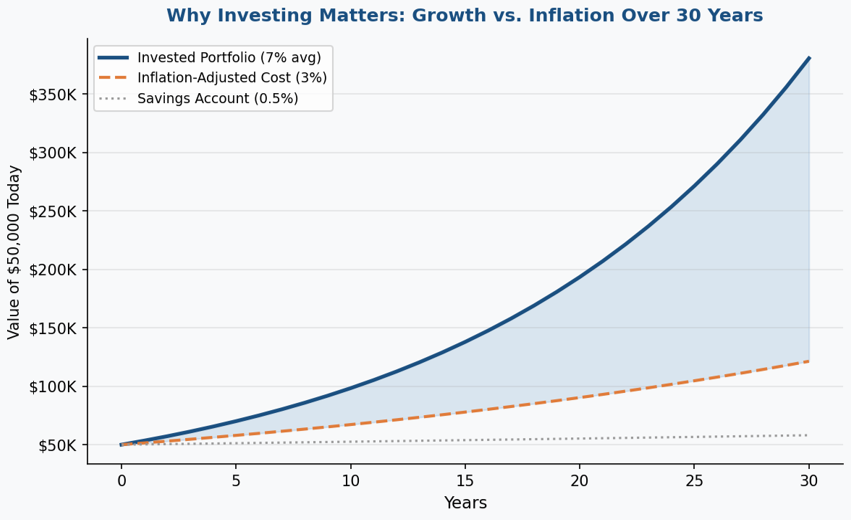

Consider this: over a 30-year period, an investment portfolio with a balanced mix of stocks and bonds can potentially grow significantly more than a traditional savings account. Historically, the average annual return of the S&P 500 has been around 7 to 10%, while the average interest rate on a savings account hovers around 0.05%. The difference is substantial, especially when you consider the impact of inflation.

The Impact of Inflation on Your Retirement

Inflation is often referred to as the silent killer of retirement savings. It gradually reduces the purchasing power of your money, meaning that the $50,000 you save today will not have the same value 20 years from now.

Over the past century, the average inflation rate in the U.S. has been about 3% annually. This might not seem like much, but over time, it can have a significant impact on your savings. If you plan to retire in 20 years, a 3% inflation rate means that prices will roughly double by the time you retire. If you are living on a fixed income, this can be devastating. The $50,000 you need annually to cover your expenses today will require approximately $90,000 annually in 20 years to maintain the same standard of living.

The Role of a Strategic Investment Plan

A well-crafted investment plan can help you combat the effects of inflation. By investing in a diversified portfolio, you can earn returns that outpace inflation, ensuring your savings maintain their value over time.

• Stocks: While they come with higher risk, stocks have historically provided higher returns, making them a key component of any long-term retirement strategy.

• Bonds: Bonds offer stability and income, helping to balance the volatility of stocks and provide a steady stream of income during retirement.

• Real Assets: Investing in assets like real estate or commodities can also provide a hedge against inflation, as these assets often increase in value as prices rise.

How Personal Financial Planning Can Help

Navigating the complexities of investing and inflation requires more than just basic knowledge. It requires a comprehensive financial plan. Here is how personal financial planning can help you mitigate the impact of inflation:

• Customized Strategies: A financial planner can develop an investment strategy tailored to your goals, risk tolerance, and time horizon, ensuring your plan is aligned with your retirement needs.

• Regular Adjustments: Life changes, and so should your plan. Regular reviews and adjustments help keep your investment strategy on track, even as market conditions and your personal circumstances evolve.

• Inflation-Proofing: A financial planner can help you build an inflation-proof retirement plan, incorporating investments that are likely to grow in value as the cost of living increases.

Inflation is a reality we cannot ignore, but with a solid investment strategy, you can protect your retirement savings and ensure a comfortable future.

At KLD Wealth Management, building an investment strategy designed to work in your favor over the long haul is central to every client relationship. Do not let inflation erode your hard-earned money. Start planning today.