10 Ways Tax Planning Maximizes Retirement Savings

When it comes to building wealth and securing a comfortable retirement, tax planning is often the unsung hero. Most people focus almost entirely on investment returns when they think about building wealth. But taxes are often the bigger lever. A portfolio that earns 8% and loses 3% to unnecessary taxes is underperforming a 7% portfolio with a smart tax strategy.

For Gen Xers with retirement on the horizon, the time to close that gap is now.

1. Tax-Advantaged Accounts: Harnessing the Power of Compound Growth

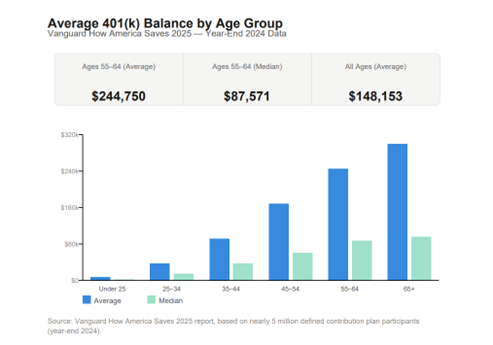

Tax-deferred accounts like a 401(k)s and IRAs allow your investments to grow without the annual drag of taxes. The effect of this compounds over time where more of your money stays invested and keeps working. According to Vanguard, the most recent average 401(k) balance for people between 55 and 64 was $244,750 in 2024. A disciplined, tax-efficient approach can push that number significantly higher.

2. Roth Conversions: Future-Proofing Your Retirement

Converting a traditional IRA to a Roth IRA means paying taxes now in exchange for tax-free withdrawals later. This strategy can be particularly powerful if you anticipate being in a higher tax bracket in retirement. A well-timed Roth conversion can save you tens of thousands in taxes over your lifetime.

3. Asset Location: Strategically Placing Investments

Different types of accounts (taxable, tax-deferred, tax-free) have different tax treatments. It's not just what you own, it's where you hold it. High-growth investments work best in tax-free accounts like a Roth IRA. Income-generating assets, which are taxed annually, are better suited for tax-deferred accounts. Getting this right can improve your after-tax returns without changing your overall portfolio.

4. Tax-Loss Harvesting: Turning Losses into Opportunities

Tax-loss harvesting involves selling losing investments to offset gains in other areas, reducing your overall tax liability. Volatile markets aren't entirely bad news. When investments decline in value, selling those positions can generate a loss that offsets gains elsewhere, reducing your overall tax bill. Done thoughtfully, this strategy turns short-term setbacks into long-term savings.

5. Charitable Giving of Appreciated Assets

Rather than writing a check to your favorite charity, consider donating stock or other appreciated assets directly. This can offer a double benefit. You skip the capital gains tax on the appreciation and still receive a charitable deduction for the full market value. The IRS reported that the average charitable deduction for itemizing taxpayers was $4,928 in 2020—donating appreciated assets can push that impact much further.

6. Managing Required Minimum Distributions (RMDs): Avoiding Penalties

Once you reach age 73, the IRS requires you to begin withdrawing from traditional retirement accounts each year. Missing a distribution results in a hefty 25% penalty on the amount not withdrawn. Planning ahead allows you to manage these withdrawals in a way that doesn't unnecessarily push you into a higher bracket.

7. Health Savings Accounts (HSAs): A Triple Tax Advantage

Few financial tools offer what an HSA does: contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are also tax-free. With Fidelity estimating that a 65-year-old couple will need about $315,000 for healthcare in retirement, building an HSA balance now is one of the smartest moves available.

8. Estate Planning: Passing Wealth Tax-Efficiently

A well-structured estate plan ensures your wealth passes to the right people with minimal tax friction. Trusts, charitable bequests, and annual gifting strategies can all reduce the tax burden on your heirs and give you more control over how your legacy takes shape.

9. Capital Gains Timing

Holding an investment for more than a year before selling qualifies you for lower long-term capital gains rates—currently 15% for most taxpayers, compared to a top short-term rate of 37%. Knowing when to sell, and in what tax year, is a basic but powerful part of any investment strategy.

10. State Tax Considerations

Where you live affects how much you pay. Several states have no income tax at all, and others offer favorable treatment for retirees. If you have flexibility in where you retire, factoring in state taxes could save thousands of dollars every year.

Tax efficiency isn't a one-time fix—it's an ongoing practice that pays off over years and decades.

A Note on Common Mistakes

Even with the best intentions, a few mistakes show up repeatedly:

Waiting too long to plan for RMDs, then getting hit with unexpected tax bracket increases

Underestimating healthcare costs and being unprepared for their full tax impact

Holding the wrong assets in the wrong accounts, costing money every year in unnecessary taxes

A tax-efficient retirement plan isn't complicated—but it does require intentionality. Let's build one around your situation.

A tax-efficient retirement plan isn't complicated—but it does require intentionality. Let's build one around your situation.