The Investor's Guide to Tax-Efficient Asset Management

Taxes and investments do not have to be a losing game, but without the right strategies, you could end up giving away a lot more than you should. This is where tax-efficient investing comes in. By carefully planning how and where your assets are allocated and sold, you can reduce your tax burden and keep more of your money working for you.

For Millennials and Gen Xers, this topic is more relevant than ever. With the historic $68 trillion wealth transfer expected from Baby Boomers, understanding tax-efficient asset management is crucial to preserving and growing your wealth. Whether you are preparing to receive an inheritance or want to optimize your existing portfolio, this guide will walk you through the key strategies you need to know.

Tax-Efficient Asset Location

One of the most critical strategies for tax-efficient investing is knowing where to hold different types of investments. This is called tax-efficient asset location, and it involves placing the right investments in the right types of accounts to reduce your overall tax bill.

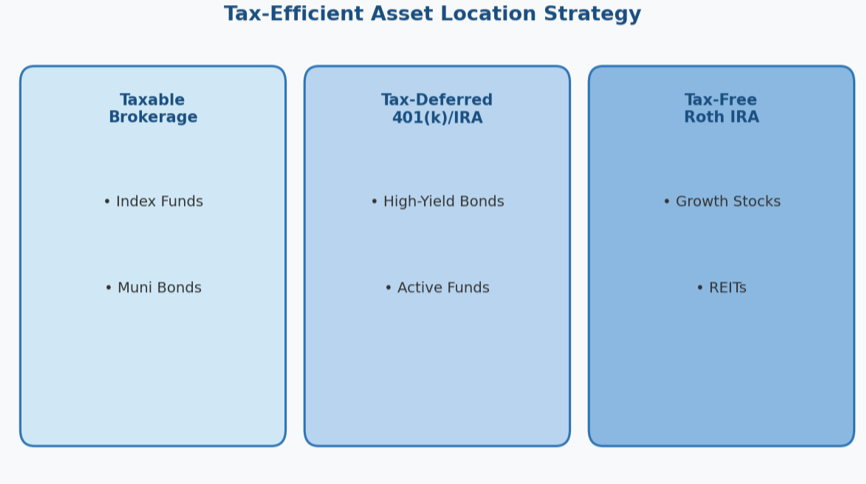

Matching the Right Investments to the Right Accounts

• High-Yield Bonds and Actively Managed Funds: These investments generate a lot of taxable income and are better suited for tax-deferred accounts like a Traditional IRA or 401(k). That way, the income is not taxed annually and can grow tax-deferred until you need it in retirement.

• Tax-Efficient Investments: Index funds, tax-managed funds, and municipal bonds are more suitable for taxable accounts. Index funds tend to have lower turnover and generate fewer capital gains, and municipal bonds often carry interest income that is exempt from federal taxes.

• Growth Stocks: Consider holding growth-oriented stocks in tax-free accounts like a Roth IRA, where you will not face capital gains taxes when you sell them. All the growth will be yours to keep.

By understanding which types of investments belong in each account type, you can reduce your overall tax burden. Asset location can seem complex, but the benefits of tax efficiency over time are well worth the effort.

Implementing Tax-Loss Harvesting

Tax-loss harvesting is a powerful strategy that turns market downturns into opportunities for tax savings. It involves selling investments that have declined in value to offset capital gains from profitable investments, effectively lowering your tax bill.

How It Works in Practice

Tax-loss harvesting works by selling an investment at a loss to offset gains from other investments you sold at a profit. For example, if you sold a stock and realized a $10,000 gain but sold another investment for a $7,000 loss, you will only be taxed on the $3,000 net gain. This strategy can help reduce your taxable income and lower your tax bill for the year.

To stay invested in the market and avoid missing potential gains, replace the sold investment with a similar but not substantially identical asset. This maintains your overall investment strategy while taking advantage of the tax benefit.

The Wash-Sale Rule

The IRS wash-sale rule prohibits you from repurchasing the same or a substantially identical investment within 30 days before or after the sale. If you violate this rule, the tax benefit is disallowed. Instead of buying the same stock or fund, look for a similar investment that has a different structure but provides comparable market exposure.

Who Benefits the Most from Tax-Loss Harvesting?

Tax-loss harvesting is most effective for investors in higher tax brackets or those who have a lot of capital gains to offset. It is particularly beneficial for Millennials and Gen Xers who might be building substantial portfolios and facing large capital gains from company stock, real estate investments, or high-growth assets.

Roth Conversions and Tax Bracket Management

Roth conversions are a powerful tool to reduce your future tax burden. By strategically converting assets from a Traditional IRA or 401(k) into a Roth IRA, you pay taxes now and enjoy tax-free growth and withdrawals later. This strategy is particularly effective for those who may be in a lower tax bracket now than they expect to be in retirement.

Tax Bracket Management: Timing Is Everything

A smart Roth conversion strategy is all about filling up lower tax brackets without pushing yourself into a higher one. For example, if you are currently in the 24% bracket, converting just enough assets to stay within that bracket can save you from paying the 32% or 35% rates later.

Combining Roth conversions with tax-loss harvesting can create a powerful one-two punch for tax efficiency. Using realized losses to minimize the tax impact of a conversion can significantly lower your taxable income in the conversion year.

Utilizing Charitable Giving for Tax Efficiency

Charitable giving is a meaningful way to support causes close to your heart, and it is also a powerful tool for tax-efficient wealth management. When done strategically, it can lower your taxable income, reduce estate taxes, and even satisfy Required Minimum Distributions.

• Donor-Advised Funds: You contribute cash, stocks, or other assets, receive an immediate tax deduction, and distribute the funds to charities over time. This allows you to spread out your giving without being rushed into choosing specific charities right away.

• Qualified Charitable Distributions: If you are 70 1/2 or older and have a Traditional IRA, you can direct up to $105,000 annually from your IRA straight to a qualified charity. QCDs can count toward satisfying your RMDs without increasing your taxable income.

• Bunching Charitable Contributions: For taxpayers who do not regularly itemize deductions, bunching contributions into a single year can help you exceed the standard deduction and maximize tax savings.

Estate Planning and Tax Minimization

Estate planning is not just about who inherits what. It is about preserving your wealth for future generations by minimizing the tax impact along the way. With a historic wealth transfer underway, Millennials and Gen Xers need to prioritize tax-efficient estate planning to ensure more of their assets pass on to loved ones.

• Strategic Asset Placement: Holding high-growth assets like stocks in a Roth IRA allows you to shield future appreciation from estate taxes, while placing income-generating assets in tax-deferred accounts can reduce immediate taxable income.

• Gifting Appreciated Securities: Instead of gifting cash, consider transferring appreciated securities to heirs in a lower tax bracket. This allows them to take advantage of their lower capital gains rate when they sell.

• Using Trusts for Tax Efficiency: Trusts can keep high-value assets out of your taxable estate. Irrevocable Life Insurance Trusts hold life insurance policies outside of your estate, while dynasty trusts allow multiple generations to benefit without additional estate taxes.

• Planning for Step-Up in Basis: Current tax laws adjust the cost basis of inherited assets to fair market value at the time of the owner's death, significantly reducing capital gains taxes for heirs. Proposed changes to this rule make proactive planning more important than ever.

Building a Comprehensive Tax-Efficient Plan

Tax-efficient investing and estate planning work best when integrated into a broader financial plan tailored to your unique goals. Here is a practical roadmap:

• Establish clear financial goals: Define what you want to achieve with your wealth, whether that is a comfortable retirement, leaving a financial legacy, or minimizing your tax burden in high-income years.

• Conduct a full portfolio review: Analyze your current investment accounts to identify where tax efficiencies can be gained. Are high-yield investments placed in the wrong accounts? Are there opportunities for tax-loss harvesting?

• Create a year-by-year tax plan: Taxes need to be managed annually to avoid costly mistakes. A multi-year plan that includes Roth conversions, tax-loss harvesting, and charitable giving ensures you are always working with your current tax bracket.

• Stay agile and adapt: Tax laws change frequently. Schedule annual reviews with your financial and tax advisors to adjust your strategy as needed.

Tax-efficient investing is not about avoiding taxes illegally or aggressively. It is about making smart, legal decisions that reduce unnecessary tax drag and preserve more of your wealth over time.

At KLD Wealth Management, this kind of integrated planning that coordinates investments, taxes, and estate strategy is exactly what the fee-only planning process is built around.