Handling the Taxation of Inherited Assets

Over the next few decades, Millennials and Generation X are set to inherit a staggering $68 trillion as Baby Boomers pass down their wealth. While this sounds like an enormous financial opportunity, inheriting assets can also come with unexpected tax complications. Many people mistakenly assume that receiving a windfall is straightforward, only to be hit with confusing tax rules and unexpected liabilities. Without a clear understanding of how different assets are taxed, you might end up losing more to taxes than you should. Different assets come with very different tax rules. Knowing those rules before you inherit or shortly after can make the difference between a windfall and a headache.

KLD Wealth Management understands that losing a parent or loved one is an incredibly difficult and emotional time. The last thing you should have to worry about is navigating complex tax decisions and financial responsibilities on your own. We’re here to help ease that burden, providing guidance and support so you can focus on what matters most.

The Basics of Inheriting Assets

When it comes to inheriting assets, not all property is treated the same from a tax perspective. Different types of assets can come with very different tax rules, and knowing the distinctions can save you a significant amount of money in the long run.

How Different Asset Types Are Taxed

Cash and Bank Accounts

Inheriting cash is the simplest form of inheritance. There’s typically no immediate tax burden on the cash itself. However, if the total estate value exceeds the federal exemption (which was $15 million in 2026), estate taxes may apply. State-level inheritance taxes are another consideration where several states have their own rules that apply regardless of the federal threshold.

Stocks, Bonds, and Investment Accounts

Here's where one of the most valuable tax benefits in the entire tax code comes into play: the step-up in basis. When you inherit investments, your cost basis resets to the fair market value on the date of the original owner's death.

What this means: if your parent or relative bought a stock at $10 per share and it was worth $100 when they passed, your basis is $100. If you sell at $110, you only owe capital gains tax on $10 not $100. Years of appreciation pass to you tax-free.

Real Estate

Inherited real estate benefits from the same step-up in basis. If you sell shortly after inheriting the property, capital gains taxes may be minimal or nonexistent. If you hold it, future appreciation will be taxable from the stepped-up basis forward. Renting the property adds another layer—rental income is taxable, and depreciation calculations become more complex.

Retirement Accounts (IRAs and 401(k)s)

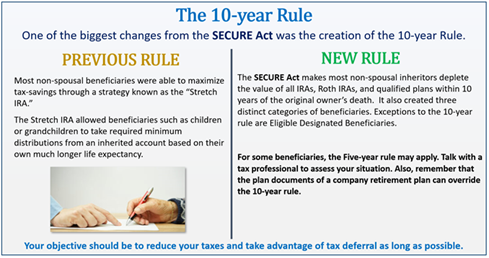

Inheriting a retirement account comes with a unique set of rules. They don't receive a step-up in basis. Withdrawals from traditional IRAs and 401(k)s are taxed as ordinary income the same as they would have been for the original owner.Under the SECURE Act of 2019, most non-spouse beneficiaries must withdraw the entire account within 10 years of the original owner's death. That compresses what could have been decades of tax-deferred growth into a much shorter, potentially tax-heavy window. Roth IRAs are more favorable where withdrawals are still tax-free, but the 10-year rule still applies.

Business Interests

Inheriting part or all of a business is typically the most complex scenario. Valuation, estate taxes, ongoing income, and exit planning all intersect. If family members have different roles or interests in the business, disputes can also arise. Working with both a tax advisor and an estate attorney early is essential.

Common Mistakes That Cost Heirs Money

• Misreporting the cost basis on inherited investments: this leads to overpaying capital gains taxes on gains that don't technically exist under the step-up rules.

• Taking large retirement account distributions in a single year: this can spike your income, push you into a higher bracket, and result in a much larger tax bill than necessary.

• Assuming state taxes don't apply: several states have inheritance or estate taxes that operate independently of the federal exemption.

• Selling inherited real estate without confirming the new basis: the step-up must be properly documented and applied.

• Not accounting for future tax law changes: the step-up in basis has been the subject of proposed reforms and could change.

Strategies Worth Considering

Plan Before the Transfer Happens

If you know an inheritance is coming, talk to a financial advisor at KLD now. There may be opportunities to gift assets before death, establish trusts, or restructure accounts in ways that reduce the eventual tax impact significantly.

Use Trusts Strategically

Certain trusts: Charitable Remainder Trusts, Dynasty Trusts, and others can shield assets, reduce estate and income taxes, and help ensure wealth passes to the right people over time. These aren't just for the ultra-wealthy; they're useful for anyone with a significant estate or complex family situation.

Spread Out Retirement Account Withdrawals

Rather than emptying an inherited IRA in one or two years, talk to a planner and map out a 10-year withdrawal strategy. This spreads the income and the taxes over time and reduces the risk of being pushed into a much higher bracket.

Consider Life Insurance for Liquidity

When an estate is concentrated in illiquid assets like real estate or a family business, heirs may need to sell something they'd rather keep just to cover taxes. Life insurance can provide the cash to cover that bill without forcing a rushed sale.

The wealth transfer happening over the next few decades is historic in scale. What you do in the first year after inheriting assets can affect your financial picture for decades.

Every inheritance situation is different. The sooner you understand what you're working with, the more options you have. Reach out and let's start the conversation.