The Hidden Retirement Power of the Tax Control Triangle

The term "Tax Control Triangle" might not come up often at the dinner table, but when it comes to retirement planning, it is one of the most powerful strategies you can use. Imagine having a plan that allows you to decide how much you pay in taxes, when you pay them, and how you can keep more of your money working for you in retirement.

If you are a Millennial or Gen Xer thinking about the future, mastering the tax control triangle should be on your radar. With concerns about rising taxes and financial stability in retirement, understanding how to manage taxes strategically can make all the difference in how long your savings last.

What Is the Tax Control Triangle?

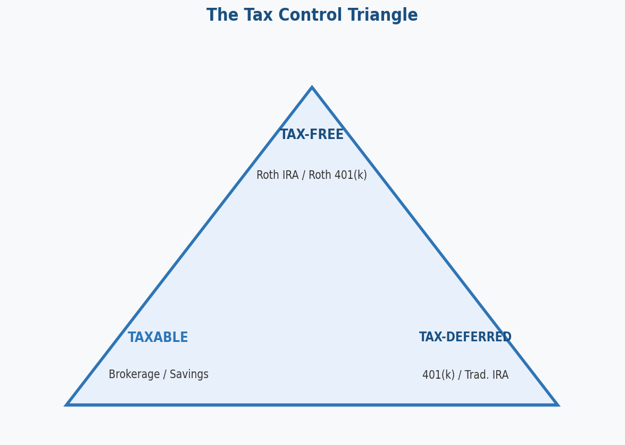

The tax control triangle refers to the three main types of accounts you can use to save and invest for retirement, each with its own unique tax treatment.

• Taxable Accounts: These include brokerage and regular savings accounts. You are taxed on interest, dividends, and capital gains in the year they are earned.

• Tax-Deferred Accounts: 401(k)s, Traditional IRAs, and similar accounts. You will not pay taxes on contributions or gains until you withdraw the money in retirement. Withdrawals are then taxed as ordinary income.

• Tax-Free Accounts: Roth IRAs and Roth 401(k)s. You pay taxes upfront on your contributions, but any future growth and qualified withdrawals in retirement are completely tax-free.

Each of these accounts plays a different role in your retirement plan, and the real power comes from how you use them together.

The Power of Strategic Withdrawals

One of the biggest decisions you will face in retirement is figuring out where your money should come from and when. This decision is more important than most people realize because the order and timing of your withdrawals can drastically impact how much you pay in taxes.

The Importance of Withdrawal Timing: The goal is to withdraw from your accounts in a way that minimizes your taxable income each year. For example, if you are withdrawing large sums from your 401(k) or IRA, you could push yourself into a higher tax bracket and pay more in taxes than necessary. By carefully planning when to tap into each account type, you can avoid these tax jumps and keep more of your income.

Blending Withdrawals for Tax Efficiency: Instead of pulling from just one account type, a common strategy is to blend withdrawals from taxable, tax-deferred, and tax-free accounts to keep your taxable income low. Withdrawing from your Roth IRA for some of your income, for example, can help you avoid moving into a higher tax bracket.

A Concrete Example

Consider two individuals, each with $600,000 saved and each withdrawing $50,000 per year as single filers in the 12% federal tax bracket.

The first, Charlie, has everything in a pre-tax 401(k). Every dollar he withdraws is taxed as ordinary income, resulting in roughly $6,000 in federal taxes per year.

The second, Dave, worked with a financial planner and used the tax control triangle. His $600,000 is split evenly across taxable, Roth, and deferred accounts. By drawing strategically from each, Dave pays only about $1,980 in federal taxes. That is a savings of over $4,000 per year on the same income.

How the Tax Control Triangle Impacts Retirement Income

Stretching Your Savings: Managing withdrawals across all three account types can extend the life of your savings by several years. By reducing the tax bite on your withdrawals, you increase the longevity of your retirement portfolio.

Reducing the Impact of Required Minimum Distributions: Once you hit age 73, you will be required to take Required Minimum Distributions from your tax-deferred accounts. These withdrawals are taxable and can push you into a higher bracket. The solution is Roth conversions and careful planning well ahead of RMD age. By converting some IRA funds to a Roth before you hit 73, you can reduce the impact of these required withdrawals and avoid a tax spike.

Practical Steps to Maximize the Tax Control Triangle

• Diversify your retirement accounts early: Contribute to a mix of taxable, tax-deferred, and tax-free accounts while you are still building savings.

• Consider Roth conversions: A Roth conversion moves funds from a tax-deferred account to a tax-free Roth. You pay taxes now but avoid paying potentially higher taxes later. The best time is often before your income peaks or during lower-income years.

• Manage taxable accounts efficiently: Use strategies like tax-loss harvesting, hold investments for the long term, and avoid short-term capital gains to keep your tax liability low.

Common Pitfalls and How to Avoid Them

Failing to Diversify: Relying too heavily on tax-deferred accounts like 401(k)s can lead to large tax bills in retirement. Spread your contributions across different account types for flexibility.

Waiting Too Long: Do not wait until retirement to think about taxes. Starting early allows you to take advantage of strategies like Roth conversions and properly balance your accounts before RMDs begin.

Overlooking Roth Conversions: Many people do not convert their IRA funds to Roth IRAs early enough, missing the chance to reduce future tax burdens. Consider this move sooner rather than later.

How Financial Planning Helps You Navigate the Tax Control Triangle

Navigating the complexities of the tax control triangle is much easier with a financial planner by your side. A planner can help you optimize how you contribute to and withdraw from each account type, ensuring your retirement is as tax-efficient as possible. At KLD Wealth Management, building a personalized, tax-efficient withdrawal strategy is a core part of the retirement planning process.

The tax control triangle offers one of the most powerful tools for securing a tax-efficient retirement. The earlier you start planning, the more you can benefit.