Is Where You Live Killing Your Retirement? Unveiling the Hidden Costs of State and Local Taxes

Did you know that the place you call home could be quietly draining your retirement savings without you even realizing it? While you might be diligently contributing to your 401(k) and carefully planning your golden years, state and local taxes, along with other "stealth taxes," could be undermining your efforts.

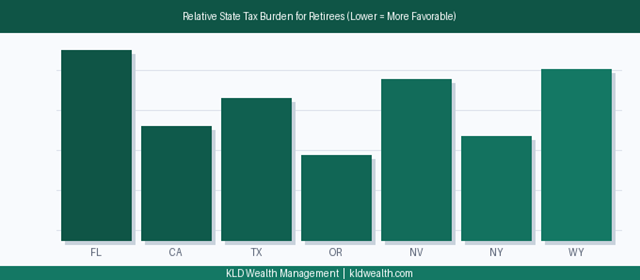

Understanding these often-overlooked financial burdens is crucial for protecting your financial future. At KLD Wealth Management, location-based tax planning is a regular part of our conversations with clients who have flexibility in where they retire.

State and local taxes vary dramatically across the country. A thoughtful location strategy can save a retiree tens of thousands of dollars over a 20-year retirement.

The Impact of State and Local Taxes on Your Retirement

State Income Taxes

State income tax rates vary dramatically. Some states, like Florida, Texas, and Nevada, have no state income tax at all, while others, such as California and Oregon, have top income tax rates exceeding 10%. These taxes apply to wages, dividends, interest, and retirement income depending on the state's tax laws.

Impact on Retirement

Higher state income taxes mean less disposable income during your retirement years. Consider two hypothetical retirees, Jane and Bob:

• Jane's Situation: Jane lives in Florida, a state with no income tax. She receives $60,000 annually from her pension and retirement accounts. Because Florida has no state income tax, she keeps the entire $60,000, subject only to federal taxes.

• Bob's Situation: Bob resides in California, which has one of the highest state income taxes in the nation. California's state income tax rate for his income level is approximately 9.3%. This means Bob pays about $5,580 in state income taxes each year, reducing his net income to $54,420 before federal taxes.

Over a 20-year retirement, Bob would pay around $111,600 in state income taxes — money that Jane could use for other purposes.

Actionable Tip

• Evaluate State Tax Policies: If you're considering relocating for retirement, research the state income tax rates and how they apply to retirement income. Some states exempt certain types of retirement income, like Social Security benefits or pensions.

• Consider Tax-Friendly States: States like Florida, Texas, Nevada, Washington, South Dakota, Wyoming, and Alaska have no state income tax, which could result in significant savings over the course of your retirement.

Property Taxes

Property taxes are levied by local governments and vary widely — not just between states but between counties and municipalities within the same state. Suppose you own a home valued at $300,000:

• In New Jersey, which has one of the highest average property tax rates at around 2.13%, you would pay approximately $6,390 annually in property taxes.

• In Alabama, with an average property tax rate of about 0.40%, your annual property tax would be roughly $1,200.

The difference is substantial — over $5,000 per year, which could be critical on a fixed retirement income.

Actionable Tip

• Research Property Tax Rates: Before deciding where to live during retirement, investigate property tax rates in various areas.

• Look for Exemptions: Many states offer property tax exemptions or reductions for seniors, veterans, or those with disabilities. Some states freeze property tax rates for seniors, preventing increases as property values rise.

• Consider Downsizing: Moving to a smaller home or a less expensive area can reduce your property tax burden.

Sales Taxes

The combined state and local sales tax rates can range from zero in states like Delaware, Montana, New Hampshire, and Oregon to over 9% in states like Tennessee, Arkansas, and Louisiana. Imagine you spend $30,000 annually on taxable goods and services:

• In Tennessee, with a combined average sales tax rate of 9.55%, you would pay approximately $2,865 in sales taxes each year.

• In Oregon, which has no sales tax, you would pay $0 in sales taxes — effectively saving $2,865 annually.

Over a 20-year retirement, this difference amounts to $57,300.

Actionable Tip

• Be Mindful of Sales Tax Rates: When budgeting for retirement, consider the sales tax rates of the states you're considering. Lower sales taxes can help stretch your retirement dollars further.

• Plan Major Purchases Strategically: If you live near a state with lower sales taxes, it may be cost-effective to make significant purchases there.

• Utilize Tax Holidays: Some states offer tax-free weekends or holidays for specific items like school supplies or energy-efficient appliances.

Estate and Inheritance Taxes

At the federal level, estate taxes apply only to estates exceeding $12.92 million. However, several states impose their own estate or inheritance taxes with much lower exemption thresholds.

States with Estate Taxes: Connecticut, District of Columbia, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington.

States with Inheritance Taxes: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

Suppose you have an estate valued at $3 million:

• In Oregon, with an estate tax exemption of $1 million, your estate would be subject to state estate taxes on $2 million. Depending on the tax rate, your heirs could lose a significant portion of their inheritance to state taxes.

• In Florida, which has no state estate or inheritance tax, your heirs would not face any state-level taxes on their inheritance.

Actionable Tip

• Incorporate Estate Planning Strategies: Work with an estate planning attorney or financial planner to minimize estate and inheritance taxes. Strategies may include:

• Gifting: Reduce the size of your taxable estate by making gifts to heirs during your lifetime, within the annual gift tax exclusion limits ($17,000 per recipient)

• Trusts: Establish trusts, such as irrevocable life insurance trusts or charitable remainder trusts, to remove assets from your taxable estate.

• Life Insurance: Use life insurance policies to provide liquidity for paying any estate taxes, ensuring your heirs receive the intended amounts.

• Consider Relocation: If estate or inheritance taxes are a significant concern, you might consider residing in a state without these taxes.

Uncovering "Stealth Taxes" That Erode Your Savings

Social Security Taxes

While the federal government may tax up to 85% of your Social Security benefits depending on your income level, certain states add an additional burden on top of that. As of now, thirteen states tax Social Security benefits to varying degrees, including Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont, and West Virginia.

For example, if you're receiving $20,000 annually in Social Security benefits and your state taxes 5% of that amount, you're losing $1,000 each year. Over a 20-year retirement, that's $20,000 less in your pocket.

Taxes on Retirement Income

Beyond Social Security, other sources of retirement income — pensions, 401(k) distributions, traditional IRA withdrawals, and annuities — may also be subject to state taxes. States like Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming have no state income tax, which can result in significant savings.

Healthcare-Related Taxes

The Affordable Care Act introduced a 3.8% Net Investment Income Tax for individuals with higher incomes. Some states have higher sales taxes on medical equipment or do not exempt prescription medications from sales tax. The average couple retiring today is expected to spend over $300,000 on healthcare throughout retirement, not including long-term care. Additional taxes can inflate this figure further.

Consider investing in Health Savings Accounts (HSAs) if you're eligible, as they offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Inflation and Cost of Living

Inflation acts as a stealth tax by eroding your purchasing power over time. With a 3% annual inflation rate, $50,000 today will have the purchasing power of approximately $37,200 in ten years. A retirement plan that doesn't account for inflation is a plan that quietly falls short over time.

Actionable Steps to Protect Your Retirement

Evaluate Your Current Location

Use online tools like the Tax Foundation and Kiplinger to compare state and local taxes across different regions. When evaluating, consider:

• Income Taxes: Determine how your retirement income sources will be taxed in your state. Some states exempt Social Security benefits, pensions, or retirement account withdrawals.

• Property Taxes: Investigate the property tax rates in your area and potential exemptions for seniors.

• Sales Taxes: Understand the combined state and local sales tax rates and how they affect your cost of living.

Consider Relocation

If feasible, relocating to a tax-friendly state can result in significant savings. Consider all factors including proximity to family, climate, healthcare facilities, and lifestyle preferences.

Pros of Relocating:

• Lower or no state income taxes, resulting in higher net income.

• Reduced property and sales taxes, lowering overall expenses.

• Potential for a lower cost of living, allowing your savings to stretch further.

Cons of Relocating:

• Moving costs and the hassle of uprooting.

• Distance from established social networks.

• Differences in climate or lifestyle that may not suit your preferences.

Optimize Your Tax Strategy

• Tax-Efficient Withdrawals: Determine the most tax-efficient order to withdraw from your retirement accounts. For example, withdrawing from taxable accounts before tax-deferred accounts can reduce your taxable income in certain years.

• Roth Conversions: Consider converting traditional IRA or 401(k) funds to a Roth IRA, especially in years when your income is lower. While you'll pay taxes on the conversion amount now, qualified withdrawals in retirement will be tax-free.

• Roth IRAs: Contributions are made with after-tax dollars, but qualified withdrawals during retirement are tax-free. Roth IRAs also have no required minimum distributions (RMDs), providing more flexibility.

• Health Savings Accounts (HSAs): If you're enrolled in a high-deductible health plan, HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Update Your Estate Plan

Consult an estate planning attorney to create or update essential documents:

• Will: Specifies how your assets will be distributed and can designate guardians for minor children.

• Trusts: Can help manage your assets during your lifetime and after death, potentially reducing estate taxes and avoiding probate.

• Power of Attorney: Appoints someone to make financial or healthcare decisions on your behalf if you're unable to do so.

• Annual Gift Exclusion: You can gift up to $17,000 per recipient annually without incurring gift taxes.

• Irrevocable Trusts: Remove assets from your taxable estate, potentially reducing estate taxes.

Adjust Your Investment Portfolio

• Asset Allocation: Adjust the mix of stocks, bonds, and other assets to reflect your risk tolerance and investment horizon.

• Global Diversification: Consider including international investments to capture growth opportunities outside the U.S.

• Federal Tax-Free Municipal Bonds: Interest income from municipal bonds is generally exempt from federal income taxes. If you purchase bonds issued by your state of residence, the interest may also be exempt from state and local taxes.

Where you live is a financial decision, not just a lifestyle one. A fee-only financial planner can model the real cost of different locations before you commit.

Don't let hidden taxes and unforeseen expenses erode your retirement savings. Contact us today to create a personalized plan that safeguards your retirement.