Double the Impact: How Charitable Remainder Trusts Benefit You and the World

What if you could receive an income stream for the rest of your life and leave a meaningful legacy behind for the world? It is not some financial magic trick. It is called a Charitable Remainder Trust, and for many Millennials and Gen Xers who care about making smart financial decisions while also wanting to leave the world a little better than they found it, the CRT might just be worth a closer look.

For many people in our generation, financial planning is no longer just about accumulating wealth. We want our plans to reflect our values, whether that means supporting environmental causes, promoting education, or addressing social justice issues. CRTs let you combine savvy financial planning with meaningful charitable giving.

What Is a Charitable Remainder Trust?

Definition and Basics

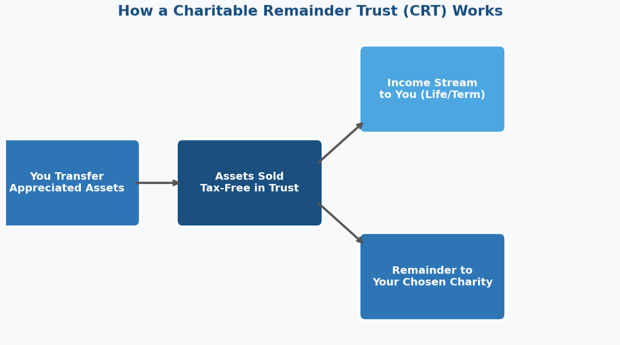

A Charitable Remainder Trust is a financial win on multiple fronts. Here is how it works: you transfer assets such as stocks, real estate, or cash into a trust, and in return, the trust pays you or designated beneficiaries an income for a set number of years or for life. After that, whatever remains in the trust goes to the charity of your choice.

There are two types of CRTs:

• Charitable Remainder Annuity Trust (CRAT): This gives you fixed annual payments based on the original value of the trust.

• Charitable Remainder Unitrust (CRUT): This provides payments that vary depending on the value of the trust's assets, which are re-evaluated annually.

Why Millennials and Gen X Should Care

If you are sitting on appreciated assets such as a home that has increased in value or a stock portfolio that has outperformed, a CRT allows you to avoid hefty capital gains taxes when you sell them. You also get a steady income stream in return. And you can support a cause that aligns with your values, leaving a legacy that truly reflects who you are.

Benefits to You: Income, Tax Advantages, and Legacy Planning

Income Stream

One of the main advantages of a CRT is that it provides you with a consistent income stream. You can designate yourself as a beneficiary and use that income for anything from retirement to travel, or even starting a new venture.

Tax Benefits

Here is where the real value becomes apparent. Let's say you have stock you bought years ago that is now worth significantly more. Normally, selling it would result in capital gains taxes that could take a sizable chunk out of your profits. By placing it in a CRT, you avoid those capital gains taxes and still receive a charitable tax deduction based on the remainder that will eventually go to charity.

For those concerned about estate taxes, CRTs can also help reduce your taxable estate. A 2023 report by Giving USA found that charitable donations through trusts like CRTs have been rising steadily, especially among those who want to avoid estate taxes and maximize their charitable impact.

Legacy Planning

A CRT allows you to leave a lasting legacy. It is not just about writing a check to a charity once. You are creating something that can support causes for generations, whether that is a local food bank, global climate initiatives, or an educational scholarship fund.

Benefits to the World: Making a Difference

Consider a Gen X couple who had always dreamed of supporting wildlife conservation. By setting up a CRT, they were able to donate a portion of their appreciated real estate to a trust. Now, they receive a steady income while knowing that, down the line, those assets will fund conservation efforts.

Millennials and Gen Xers are more philanthropic than ever. According to a 2020 study by Fidelity Charitable, 71% of Millennials prioritize purpose over profit, actively seeking ways to align their investments with their values. CRTs offer an excellent structure for making that happen in a meaningful, long-term way.

How to Set Up a CRT

Choosing between a CRAT and a CRUT is one of the first decisions you will make. If you want fixed payments, the CRAT may suit you better. If you prefer more flexibility and are comfortable with payments that fluctuate based on your assets, a CRUT might be the right fit.

You will also want to consider how long the income payments will last, whether for your lifetime or a set number of years, and of course, choose a charity that aligns with your personal values.

Setting up a CRT is not a DIY project. It is crucial to work with a financial planner and estate attorney who can tailor the trust to fit your goals. You do not want to miss out on tax advantages or leave room for errors in the trust's setup.

A Real-Life Example

John and Emily, a Gen X couple with a rental property that had appreciated significantly, decided to sell but did not want to pay the capital gains tax. By placing the property into a CRT, they avoided those taxes, received a charitable deduction, and now enjoy regular income from the trust. Their chosen charity, a scholarship fund for underprivileged students, will eventually receive the remainder.

This setup allowed John and Emily to benefit now while ensuring their legacy would continue to make a difference long after they are gone.

How CRTs Fit into a Broader Financial Plan

A CRT should not exist in a vacuum. It works best as part of a larger financial and estate planning strategy. When combined with other tools like retirement accounts, life insurance, and living trusts, a CRT can offer even more control over your legacy and financial future. Regular reviews with your financial planner ensure that everything stays on track as your life and financial situation evolve.

A Charitable Remainder Trust offers a powerful way to double your impact. It provides financial benefits for you now while leaving a lasting legacy for the causes you care about.