5 Reasons Generation X Needs Tax Planning Now

Remember the days when you’d gather around the TV to watch “The A-Team” or rock out to Bon Jovi’s “Livin’ on a Prayer”? Just like Mr. T and the gang had a plan for every mission, Generation X needs a strategic plan for their financial future, especially when it comes to tax planning. Here are five concrete reasons why getting serious about tax planning now will make a meaningful difference when it matters most.

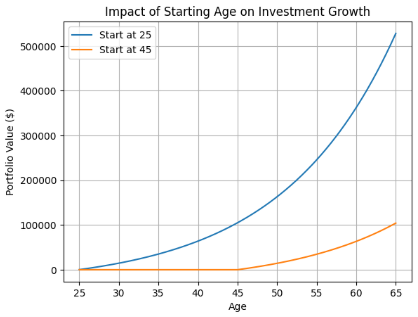

1. You're Closer to Retirement Than You Think

Retirement isn't some abstract future event anymore. It's within a 10- to 20-year window for most Gen Xers. As a member of Generation X, you’re in your prime earning years. That means every year without a tax-efficient savings strategy is a year of compound growth you won't get back. Maximizing contributions to 401(k)s and IRAs isn't just about sheltering income today; it's about letting tax-deferred growth do the heavy lifting for years to come, ensuring a more comfortable retirement.

2. Tax Laws Don't Stay Still

Tax laws are constantly evolving, and there's little reason to expect that to change. Provisions that benefit you now may not exist in five years, and new ones could catch you off guard. Staying ahead of those changes through proactive planning is far less painful than scrambling to react after the fact. A small adjustment in strategy today can sidestep a large tax hit tomorrow.

3. Asset Management Has Tax Consequences

If you’ve invested in stocks, real estate, or other assets, you need a plan to manage the tax implications. Capital gains taxes can take a real bite out of your returns if you're selling without a plan. Strategic tax planning helps you decide not just what to sell, but when and in what order, potentially saving thousands overtime without changing your overall investment approach.

4. Healthcare Is Going to Cost More Than You Expect

Healthcare costs can be a significant burden in retirement. Fidelity's most recent 2025 study found that the average 65-year-old couple retiring in 2025 will need $345,000 to cover healthcare expenses just to cover out-of-pocket healthcare costs throughout retirement. That's a sobering number, and it's one that a Health Savings Account (HSA) is uniquely built to address. HSAs offer a rare triple tax advantage: contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses aren't taxed either. By integrating HSAs into your tax planning strategy, you can better prepare for healthcare costs without unnecessary tax liabilities.

5. What You Leave Behind Matters

If you have people counting on you; a spouse, children, aging parents you're supporting, then estate planning is part of the conversation too. Without the right structure in place, a significant portion of what you've built over your lifetime could go to taxes instead of the people or causes you care about. Proper tax planning addresses this directly, through tools like gifting strategies, trusts, and beneficiary designations that ensure your wealth transfers the way you intend.

A Few Common Pitfalls Worth Avoiding

Even well-intentioned financial plans can go sideways without the right tax strategy in place:

• Over-concentration in one asset class: Diversification has tax implications too:

By diversifying your investment portfolio and considering the tax implications of each investment, you can avoid the risks associated with over-concentration in any one asset.

• Triggering a higher tax bracket by failing to manage income streams across the year: Strategic tax planning can help you manage multiple income streams more effectively, ensuring you don’t move into a higher tax bracket unnecessarily.

• Planning for Unforeseen Expenses: With a solid tax plan, you can create a financial cushion for unexpected expenses, reducing the need for high-interest loans or premature retirement withdrawals.

Tax planning isn't just for the wealthy—it's for anyone who wants to keep more of what they've earned.